The global financial system is on the brink of a major transformation. After more than five decades of operating as the backbone of international payments, SWIFT is embracing blockchain technology to modernize cross-border transactions. This shift is not just a technical upgrade—it represents a fundamental change in how money moves across the world.

The Legacy System: Why Change Is Needed

Since its establishment in 1973, SWIFT has enabled secure communication between banks for international transfers. While reliable, the system has long faced criticism for being:

- Slow (transactions can take 1–5 days)

- Costly due to multiple intermediaries

- Lacking transparency in payment tracking

As global commerce accelerates and digital economies expand, these inefficiencies have become increasingly problematic.

Enter Blockchain: A New Financial Infrastructure

Blockchain technology offers a decentralized, transparent, and faster alternative to traditional banking rails. By integrating blockchain into its ecosystem, SWIFT aims to:

- Enable near real-time cross-border payments

- Reduce reliance on correspondent banking networks

- Increase transparency and traceability

- Lower transaction costs

Unlike cryptocurrencies such as Bitcoin, SWIFT’s blockchain initiatives are focused on regulated financial institutions, ensuring compliance with global standards.

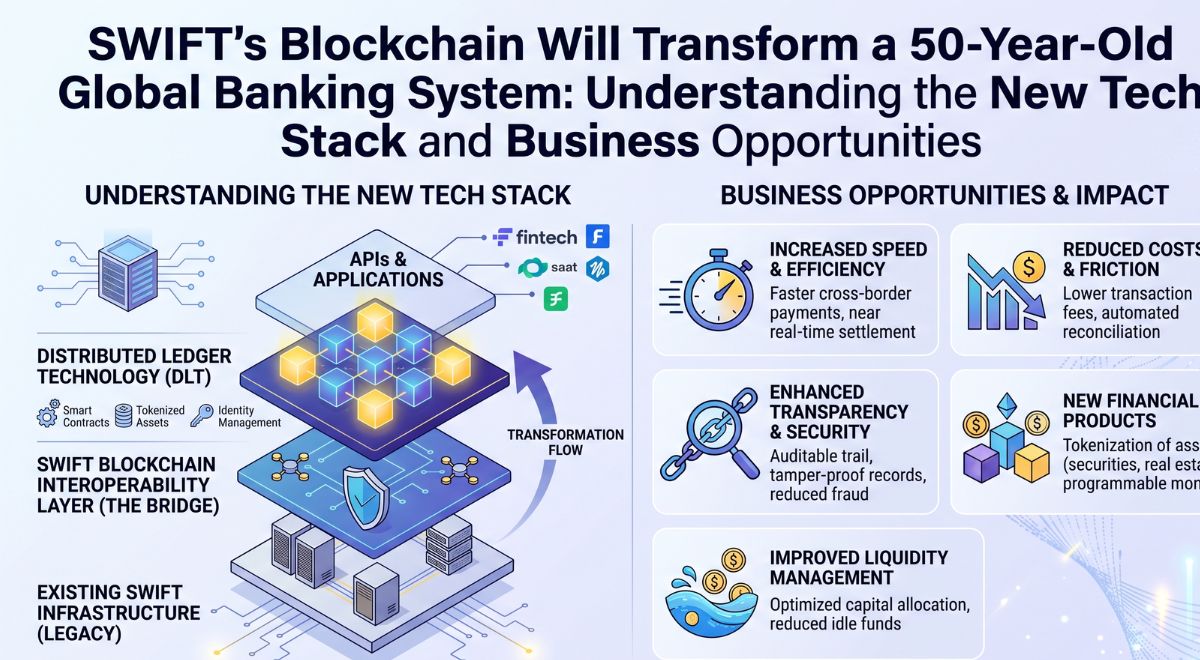

The New Tech Stack: What’s Changing?

SWIFT is not replacing its system overnight—instead, it is building a hybrid infrastructure that combines existing systems with blockchain layers. Key components of this evolving tech stack include:

1. Distributed Ledger Technology (DLT)

At the core is DLT, which allows multiple parties to share and update transaction data securely in real time.

2. Interoperability Protocols

SWIFT is developing solutions that connect different blockchains and traditional banking systems, ensuring seamless communication across networks.

3. Tokenization of Assets

Financial assets such as currencies, bonds, and securities can be tokenized, making them easier to transfer, track, and settle instantly.

4. Smart Contracts

Automated agreements executed on blockchain reduce manual processing and eliminate delays caused by intermediaries.

Business Opportunities Emerging from the Shift

This transformation opens up significant opportunities across the financial and technology sectors:

Fintech Innovation

Startups and financial technology firms can build new solutions on top of SWIFT’s blockchain-enabled infrastructure, including payment gateways and digital wallets.

Banking Efficiency

Traditional banks can reduce operational costs, improve liquidity management, and offer faster services to customers.

Cross-Border Trade Expansion

Businesses, especially SMEs, can benefit from faster and cheaper international payments, enabling smoother global trade.

New Revenue Models

Tokenized assets and programmable money create entirely new financial products and services.

Challenges and Considerations

Despite its promise, the transition to blockchain is not without hurdles:

- Regulatory uncertainty across different countries

- Integration complexity with legacy systems

- Security concerns and scalability issues

- Resistance from institutions invested in current models

SWIFT must carefully navigate these challenges to ensure a smooth transition.

The Road Ahead

SWIFT’s blockchain strategy signals a future where global payments are faster, cheaper, and more transparent. While the complete transformation may take years, early implementations are already shaping the next generation of financial infrastructure.

As the world moves toward digital finance, SWIFT’s evolution could redefine international banking—bridging the gap between traditional finance and decentralized technologies.